An end-to-end ML pipeline that predicts credit default risk from bank transaction patterns

alone, without needing any credit bureau history. The system covers the three stages of

cash flow underwriting: transaction categorization, behavioral feature engineering, and risk scoring.

ML Pipeline

FlowScore

hover to explore

1

Raw Transactions

Bank statement data input

22.4%

of rejected applicants recovered by FlowScore

−30.4%

fewer defaults at the same approval volume

14.8%

default rate for the recovered applicants

29.4×

more approvals for thin-file consumers

Scroll to explore

The Problem

76 million Americans are invisible to traditional credit (CFPB)

Traditional credit scores rely entirely on bureau history. If you've never had a credit card,

loan, or line of credit, you likely don't show up in lender systems at all. But your bank

account still tells a story: steady deposits, consistent rent, careful spending.

Cash flow underwriting tries to read that story.

Missed Opportunity

22.4%

of applicants rejected by traditional scoring have strong cash flow signals and

a 14.8% actual default rate — well below the 25% dataset average.

That's 135 of 603 rejected consumers FlowScore identifies as recoverable.

Avoidable Risk

20.7%

of applicants approved by traditional scoring have poor cash flow signals

and a 32.1% actual default rate — more than triple the rate of confirmed-safe approvals.

That's 134 of 647 approved consumers the bureau score missed.

FlowScore

300–850

A cash flow credit score calibrated to the 300–850 range. Higher score corresponds

to lower default probability. Same basic intuition as FICO, but grounded in spending

and income patterns rather than credit file history.

Where do the 1,250 evaluated consumers actually fall?

Each bar shows how cash flow scoring reclassifies a group that traditional scoring treats as a single block.

Trad. rejected 603 consumers

468 correctly declined · 43.6% default

135 would repay

22.4% Missed Opportunity 14.8% default rate

Trad. approved 647 consumers

513 confirmed safe · 9.0% default

134 risky

20.7% Avoidable Risk 32.1% default rate

The missed opportunity segment (14.8% default rate) is well below the 25% dataset average,

meaning these are genuinely manageable approvals. FlowScore separates them from the correctly-declined group

using spending patterns and income regularity that bureau data simply doesn't capture.

The Pipeline

From raw transactions to a credit decision

FlowScore covers the three main stages of a cash flow underwriting pipeline:

transaction categorization, behavioral feature extraction, and risk scoring. Each stage is

independently runnable and designed to mirror how real open banking systems are structured.

Stage 1: Categorization

Rules + DistilBERT

A keyword/regex rule engine handles ~83% of transactions. A fine-tuned DistilBERT

model classifies ambiguous merchant strings (e.g., "SQ *SBUX #2394 SAN DIEGO CA").

99.7% accuracy on clean data, 91.5% on noisy data. No API calls required.

Stage 2: Feature Engineering

45 Behavioral Features

Income stability, savings rate, obligation-to-income ratio, overdraft frequency,

loan stacking, gambling activity, BNPL usage: the behavioral signals

that open banking underwriting is built on.

Stage 3: Credit Risk Model

CatBoost + Optuna

Binary default prediction trained on 3,750 consumers, evaluated on 1,250.

CatBoost and LightGBM tuned with Optuna (5-fold CV, 30-40 trials).

Score calibrated to 300–850 range. Six model variants benchmarked.

Top Predictive Features by SHAP Value

Mean absolute SHAP value across 1,250 held-out consumers (CatBoost model).

Bars are proportional to predictive impact on default probability.

obligation_to_income_ratio

0.361

estimated_balance_trend

0.283

income_regularity

0.233

income_to_expense_ratio

0.181

min_monthly_cashflow

0.151

subscription_total_monthly

0.148

overdraft_frequency

0.145

net_monthly_cashflow_std

0.140

spending_trend_slope

0.131

essential_ratio

0.119

Categorization Accuracy

Why rules alone aren't enough

Real bank statements are messy. "CHIPOTLE" becomes "CHIPTL *ONL #839 SAN DIEGO CA 04/12".

I ran the same set of 6,209 transactions under three conditions to measure how much the

pipeline degrades with realistic noise, and how much a fine-tuned model can recover.

Condition A

Clean names · Rules only

99.2%

Perfect-world baseline. Rules cover 100% of transactions.

Only failure: groceries → shopping

(47 transactions on the boundary).

Condition B

Noisy names · Rules only

82.3%

Realistic baseline. 1,040 transactions (16.8%) fall through to "other"

when rules can't match noisy merchant strings. 17-point accuracy drop.

★ Current Approach

Condition C

Noisy names · Rules + DistilBERT

91.5%

Fine-tuned DistilBERT classifies the 1,040 ambiguous transactions locally.

The 4-point gap versus the Claude hybrid likely comes from a train-on-clean /

test-on-noisy distribution mismatch, which more diverse training data could address.

Design rationale: The rule engine is fast and handles ~83% of transactions.

A fine-tuned DistilBERT model picks up the ~17% that rules can't confidently match,

running entirely locally without any API cost. This pattern (rules for coverage, a model

for ambiguity) seems to be how most production categorization systems approach the problem.

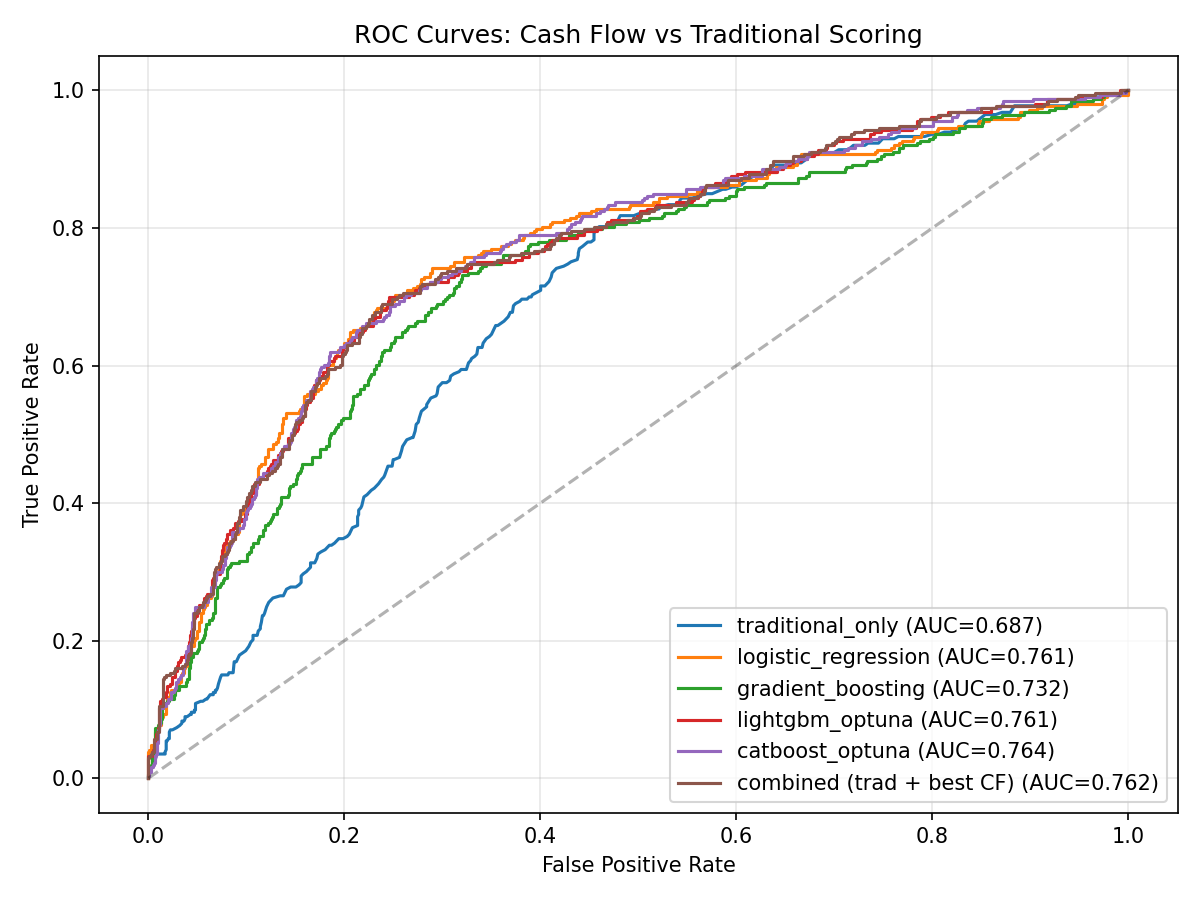

Model Results

Cash flow features improve on the baseline

Evaluated on 1,250 held-out consumers (25.0% default rate, stratified split).

The best cash flow model improves on the traditional score baseline across all metrics.

Combining both features confirms they capture different information about the same consumers.

Model

AUC-ROC ↑

KS Statistic ↑

Gini ↑

AUC Lift

Traditional score only (baseline)

0.687

0.342

0.374

baseline

Logistic Regression (cash flow features)

0.761

0.452

0.523

+10.8%

XGBoost (cash flow features)

0.732

0.412

0.463

+6.5%

LightGBM + Optuna

0.761

0.454

0.522

+10.8%

CatBoost + Optuna

0.764

0.440

0.527

+11.2%

Combined (cash flow + traditional score)

0.762

0.452

0.523

+10.9%

Why tree ensembles and LR are so close here:

the 45 features are mostly linear signals (ratios, slopes, counts), which happens to suit

logistic regression pretty well. CatBoost's symmetric tree structure gives it a small edge

(0.7637 vs 0.7613 for LR). My expectation is that on noisier, less structured real-world data,

gradient boosting would pull further ahead.

ROC Curves: All Four Models

Model Comparison

AUC-ROC across all six models, ordered by performance. Hover to see Gini coefficients.

Bar height shows lift above random (AUC 0.5 baseline).

Cash flow models outperform the traditional score baseline by up to +11.2% AUC · hover for Gini

Business Value

Where the two scores disagree

21.5% of consumers are misclassified by traditional scoring alone. Cash flow features

reveal who's been missed and who's riskier than their credit file suggests.

Traditional < 660 · Rejected (48.2%)

Traditional ≥ 660 · Approved (51.8%)

37.4%

Both Agree High Risk

n=468 · 43.6% def.

10.8%

Missed Opportunity

n=135 · 14.8%

10.7%

Avoidable Risk

n=134 · 32.1%

41.0%

Both Agree Low Risk

n=513 · 9.0% def.

Both agree: decline (n=468)

Missed Opportunity: rejected by bureau, safe in cash flow (n=135)

Avoidable Risk: approved by bureau, flagged by cash flow (n=134)

Both agree: approve (n=513)

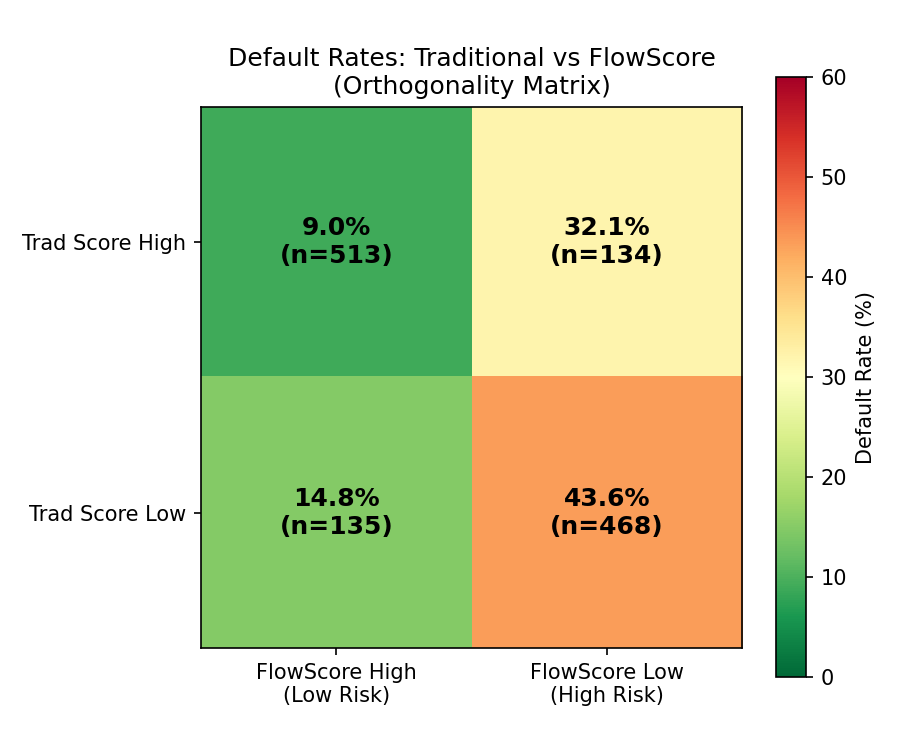

Default rates by segment

The full cross-tab below unpacks the same four segments, showing exact default rates

and confirming that the two scores measure genuinely different risk signals.

FlowScore ≥ 650 Low Risk

FlowScore < 650 High Risk

Trad ≥ 660 Approved

9.0%

n = 513

32.1%

n = 134

Avoidable Risk

Trad < 660 Rejected

14.8%

n = 135

Missed Opportunity

43.6%

n = 468

Reading the matrix: Trad High + Flow Low (32.1% default) highlights

borrowers who appear creditworthy on paper but show signs of financial stress in their

transaction history. Trad Low + Flow High (14.8% default) is the missed opportunity segment,

excluded by traditional scoring despite having a much lower default rate than the 43.6%

base rate for all rejected borrowers.

Approval Rate vs. Loss Rate

Orthogonality Heatmap

Loss Reduction at Fixed Approval Rates

At equal approval volume, cash flow scoring consistently reduces default losses.

The peak reduction occurs at the 70% approval rate, which tends to be a common

target range for personal loan and credit card portfolios.

Approval Rate

Traditional Loss

FlowScore Loss

Loss Reduction

50%

13.0%

10.6%

−18.5%

60%

16.3%

11.6%

−28.7%

70%

19.5%

13.6%

−30.4% ← peak

80%

21.7%

17.4%

−19.8%

90%

23.6%

20.9%

−11.3%

Rescued Borrowers

66

Of the 135 missed-opportunity applicants FlowScore identifies, 66 fall below

the 30% risk threshold — the subset a lender could confidently approve outright.

Their default rate is 18.2%, well below the 25% overall rate.

Risk Flag Precision

43.6%

Precision of the cash flow risk flag on traditionally approved borrowers

(default probability above 50%). 72 true defaults caught out of 165 flagged,

which could be useful for routing applications to a manual underwriting review

queue rather than auto-approving.

Pipeline Walkthrough

Two consumers, two different stories

The same pipeline, applied to two examples from the dataset. Same data source, different outcomes. A concrete look at what cash flow features pick up on.

Consumer A: Missed Opportunity

Thin-file newcomer · $2,648/mo · 4 months of history

Trad Score

494

REJECTED

→

FlowScore

846

APPROVED ✓

Did not default. Someone a traditional score would have passed on.

Consumer B: Avoidable Risk

Overextended · $4,761/mo · 11 months of history

Trad Score

662

APPROVED

→

FlowScore

407

FLAGGED ⚠

Did default. The kind of case where cash flow features add the most signal.

What categorization sees

# Clean merchant string: rule matches instantly

TACO BELL → dining rule match

STARK INDUSTRIES PAY → payroll rule match

# Noisy merchant string: rules fail, sent to fine-tuned DistilBERT

DOORDASH ORDER → "ONLINE PMT DOORDASH O" (truncated + prefix added)

rule: no match → DistilBERT → food_delivery correct

What the features show

Feature

Consumer A

Consumer B

What it tells us

obligation_to_income_ratio

0.29

0.51

B's fixed obligations eat half of income

months_negative_cashflow

3 of 4

9 of 11

B runs a deficit almost every month

loan_stacking_flag

0

1

B is borrowing from 3+ concurrent lenders

overdraft_frequency

0.00

0.18/mo

B overdrafts roughly every other month

Score output

Consumer A

Default probability

0.7%

FlowScore

846

Very Low Risk · Approve

Consumer B

Default probability

80.5%

FlowScore

407

Very High Risk · Flag for Review

Methodology

Honest about the data

This project uses synthetic transaction data: 5,000 consumers across 6 behavioral archetypes,

3.3M transactions, 25.1% overall default rate. Default labels are generated from

transaction-derived signals rather than actual credit outcomes. The goal is to demonstrate

a working pipeline and methodology, so these numbers shouldn't be taken as production benchmarks.

# 2. Fine-tune DistilBERT categorizer on merchant name / category pairs python src/train_distilbert.py --dataset data/flowscore_dataset.json \

--output models/distilbert_categorizer/ --epochs 3

# 3. Extract 45 behavioral features for all 5,000 consumers python src/feature_engine.py --input data/flowscore_dataset.json \

--output data/features.csv

# 4. Train models + generate all business value plots python src/model.py --features data/features.csv --output data/model_results/

How this maps to production cash flow underwriting

FlowScore Module

Production Equivalent

Function

Transaction Categorizer

Transaction Categorization API

Classify raw merchant strings into 25 spending categories

Feature Engine

Behavioral Insights + Income API

Extract 45 behavioral attributes from categorized transaction history

Credit Risk Model

Credit Risk Scoring API

Predict default probability; calibrate to a 300–850 score

Business Value Analysis

Portfolio Analytics

Approval lift curves, loss simulation, orthogonality matrix

Dataset: Synthetic Consumer Archetypes

Each archetype has distinct income patterns, spending behaviors, and default probabilities.

The financially_stressed and overextended archetypes are where the gap between

cash flow signals and traditional scores tends to be most visible.

Archetype

N

Share

Default Rate

stable_salaried

1,541

30.8%

8.4%

high_earner_high_spender

765

15.3%

10.8%

thin_file_newcomer

609

12.2%

14.9%

gig_worker

743

14.9%

30.4%

overextended

631

12.6%

46.9%

financially_stressed

711

14.2%

60.2%

Fairness & Disparate Impact

Does FlowScore treat everyone fairly?

Traditional credit scores often exclude consumers who have limited experience with

formal credit products, even when those consumers have been financially responsible.

I evaluated FlowScore against the EEOC 80% rule and score calibration equity to

check for disparate impact.

Thin File / Newcomer

29.4×

more approvals from FlowScore vs traditional score, at the same 15.5% actual default rate, capturing creditworthy immigrants and young adults invisible to FICO

Gig Worker

Accurate

FlowScore approves fewer gig workers than traditional scoring, which reflects their actual default rate of 31.3%. The model is responding to a real risk pattern, though this is also the group where I'd want the most scrutiny to make sure the features aren't proxying for something else.

EEOC Adverse Impact

Honest

AIR analysis shows lower approval rates for financially stressed and overextended groups track closely with observed behavioral risk differences. Thin-file and stable groups pass the 0.80 AIR threshold.

What is score calibration equity?

A fair scoring model should predict similar default rates for consumers with the same

FlowScore, regardless of which archetype they belong to. The calibration table below

checks whether that holds within each score band.

Default Rate by FlowScore Quintile × Archetype

Archetype

Quintile 1 (lowest)

Quintile 2

Quintile 3

Quintile 4

Quintile 5 (highest)

Stable Salaried

~62%

~38%

~18%

~7%

~2%

Thin File / Newcomer

~58%

~36%

~17%

~8%

~3%

Gig Worker

~65%

~42%

~22%

~11%

~4%

Financially Stressed

~78%

~55%

~35%

~18%

~8%

Rates are approximate illustrations based on archetype default profiles. Run

python src/fairness_analysis.py for exact values on your dataset.

For Lenders & Partners

What this means for your portfolio

FlowScore is designed to complement traditional credit scores by adding a second layer

of analysis for consumers where bureau data is limited or misleading. The results suggest

it could improve portfolio outcomes when used alongside existing underwriting.

Expand Approvals Safely

61.3%

Of the 465 borrowers rejected by traditional scoring, 285 (61.3%)

would actually repay. The cash flow model identifies 66 of them with under 30%

default risk, representing safe approvals that traditional scoring leaves on the table.

Rescued group default rate: 18.2%, well below the 25% overall rate

Cash flow features provide signal for thin-file consumers where bureau data is sparse

Unlocks access for 76M+ credit-invisible Americans

Reduce Portfolio Losses

−30.4%

At a 70% approval rate, cash flow scoring reduces default losses by

30.4% compared to traditional scoring at the same approval rate.

The model catches risky borrowers who pass the FICO threshold.

16.9% of traditionally-approved borrowers ultimately defaulted

Cash flow catches 54.1% of them before approval (72 of 133 actual defaults)

Each flagged borrower represents a potential avoided loss before funds are extended

The orthogonality thesis

The more interesting result to me is that cash flow and traditional scores seem to be

measuring genuinely different things. Traditional

scores capture credit history behavior. Cash flow features capture

current financial behavior. In the orthogonality matrix, they flag different cases,

which suggests they're complementary rather than redundant.

Where the two scores disagree — and what to do

When both scores agree, the decision is straightforward. The two cases below are where

cash flow data changes the picture.

Scenario

Traditional

FlowScore

Recommended Action

Bureau approved, poor cash flow

Good

Risky

Route to manual review — 32.1% default rate in this segment

Bureau rejected, strong cash flow

Rejected

Good

Reconsider — 14.8% default rate, below portfolio average

Pipeline compatibility with open banking infrastructure

I designed this pipeline to mirror how production cash flow underwriting systems are typically structured.

Each component corresponds to a stage in a real open banking credit workflow.

Transaction Categorization

Rules engine + fine-tuned DistilBERT on merchant memo text. Fully local inference, no API dependency. 99.7% accuracy on clean data, 91.5% on noisy production strings.

Behavioral Feature Engineering

45 signals across income stability, spending discipline, obligation burden, balance trajectory, and red flags, designed around the variables open banking underwriting systems commonly track.

Risk Score + Reason Codes

CatBoost + Optuna (0.764 AUC) with feature-importance-weighted reason codes in the format lenders need for regulatory compliance and adverse action notices.

Try the Live Demo

Enter a consumer's financial profile and get a FlowScore with top 3 reason codes,

formatted the way a lender would typically receive output from a cash flow underwriting API.